We’ve discussed in our recent series of insights the technical feasibility, infrastructure hurdles, and current projects in utilizing H2 gas as an alternative fuel for the calcination requirements of cement production. While economic obstacles remain, early capital is increasingly helping pave a path to the market. Here, we present a review of the regulatory policies that are aimed to catalyze the development of and scaling of hydrogen fuel generation and use. It’s important to note that hydrogen fuel is still in its early stages, undergoing rapid changes with many unknowns, uncertainties, and some glimmers of potential. Here, as in all of our published insights, we are conveying observations as we find them to gain and share an understanding on the progress of this development.

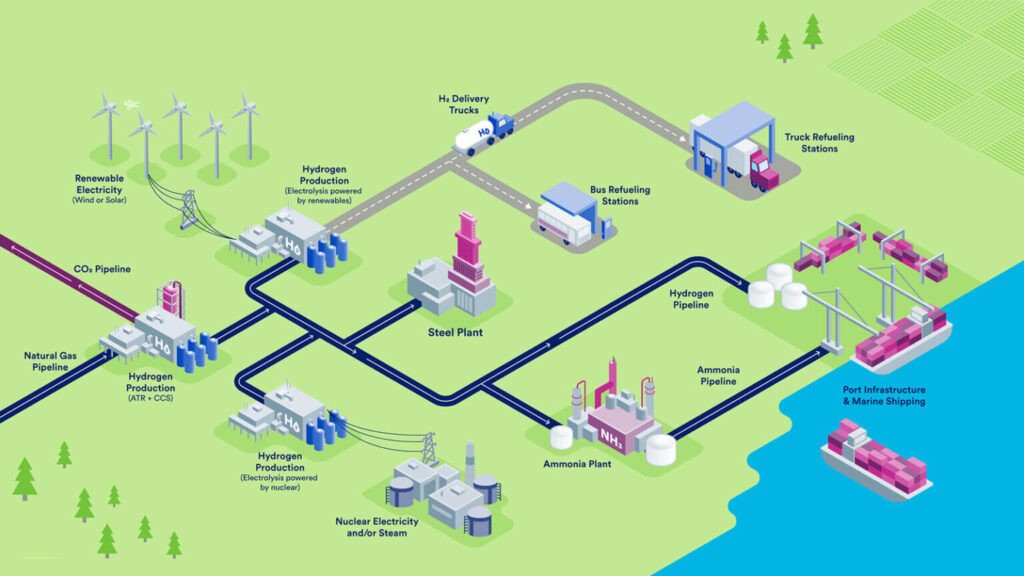

In brief overview, hydrogen fuel is currently made solely through energy intensive processes that split hydrogen-containing molecules such as water(H2O) and methane(CH4) producing molecular hydrogen in gaseous form(H2). Currently methane is the most popular source, split by Steam Methane Reforming(SMR), also emitting CO2 as a byproduct. Green hydrogen is currently claimed to be the most sustainable method, which splits water using renewable energy to produce only gaseous hydrogen and oxygen.1 Renewable energy is still limited in capacity and scale, highly demanded when available, so it’s a limiting factor of green H2 production.2

These energy input limits of H2 production suggest that it may be a smaller, yet substantial driver of industrial decarbonization. Therefore, it’s believed by some that green H2 should only be used in areas where direct application of electricity is not possible, such as cement production rather than applications like passenger cars or residential heating.3 Despite these implications, the majority of H2 fuel policy so far has focused on transport and refueling stations.4 Other areas of climate tech such as Carbon Dioxide Removal(CDR) have been more widely adopted and implemented by leaders in the cement industry as the technology has been in development decades longer than hydrogen. Given the nature of its aim to remove CO2 from the air and from emissions, it’s also perceived as a more direct approach to industrial decarbonization. CDR has seen incentivizing policy such as the US’ 45Q tax credits, started in 2008, that allow organizations to redeem $60-180 per ton of CO2 captured, depending on whether it’s stored/utilized and whether captured from ambient air or directly from emissions sources.5,6

Recent policy changes are beginning to support expansion of H2 fuel generation and adoption with the US’ 45V hydrogen tax credits, akin to 45Q carbon credits. Established in 2022 under the Inflation Reduction Act, 45V provides a tax credit of up to $3 per kilogram of H2 to projects with “low lifecycle greenhouse gas emissions.”7 In December of 2023, the US Treasury and IRS published a Notice of Public Rulemaking(NPRM), which clarified means of 45V credit redemption for existing and prospecting H2 producers. The NPRM included directions on how producers should calculate their lifecycle greenhouse gas emissions using 45VH2-GREET, the H2 production version of the Department of Energy’s(DOE) existing R&D GREET model. The NPRM also proposes means to ensure that emissions from electricity generated to drive electrolysis H2 production are within state guidelines to prevent production from increasing overall grid emissions.

The US government also introduced Bipartisan Infrastructure Law funding of $8 billion for a Regional Clean Hydrogen Hubs Program.8 Seven regional hubs were selected to receive $7 billion in of the funds with the aim to drive the US market toward low-cost, H2 production:

- Mid-Atlantic Hydrogen Hub ( Pennsylvania, Delaware, New Jersey)

- Appalachian Hydrogen Hub (West Virginia, Ohio, Pennsylvania)

- California Hydrogen Hub

- Gulf Coast Hydrogen Hub (Texas)

- Heartland Hydrogen Hub (Minnesota, North Dakota, South Dakota)

- Midwest Hydrogen Hub (Illinois, Indiana, Michigan)

- Pacific Northwest Hydrogen Hub (Washington, Oregon, Montana)

The federal investment will work in junction with about $40 billion in private investment, and the administration claims that “roughly two-thirds of total project investment are associated with green (electrolysis based) production, within the hubs.”8 It’s stated that the remaining $1 billion will be used to fuel H2 demand by catalyzing innovation in H2 use. The administration also states that “The hubs are covered under the Justice40 Initiative, which aims[emphasis added] to ensure that 40 percent of the overall benefits of certain federal investments flow to disadvantaged communities that are marginalized by underinvestment and overburdened by pollution. Hubs have also submitted detailed Community Benefits Plans, including how the project performers will transparently communicate, eliminate, mitigate, and minimize risks.”8

DOE has announced other resources supporting research and development (R&D) in clean hydrogen technology through several initiatives. Their “Hydrogen Hub Matchmaker” program aims to connect clean hydrogen producers, end-users, and other stakeholders to facilitate the development of infrastructure networks for production, storage, and transportation. Another program, with $500 million in funding, supports American manufacturing of clean hydrogen equipment and explores approaches to recycling these technologies, potentially strengthening domestic supply chains for key components.

Hydrogen infrastructure policy is also showing increasing support internationally. China, the world’s top hydrogen producer, aims for large-scale adoption through its “Hydrogen Industry Development Plan,” targeting significant production and a massive increase in hydrogen fuel cell vehicles on the road by 2025.9 The United Arab Emirates has developed a Hydrogen Leadership Roadmap, with goals of exporting of low carbon hydrogen, and H2 derivative products to importing regions; and supporting new derivatives through low-carbon steel, “sustainable kerosene”, and other industries.10 Europe is also joining the race, with the EU’s Hydrogen Strategy focusing on clean hydrogen development. The strategy includes tax breaks, funding programs, and the establishment of regional hubs to stimulate production, infrastructure creation, and collaboration across the continent.11

Incentivizing policy is growing across the board in support of H2 fuel use and production, and the financial commitments by the governments of many regions are a sign of increasing belief in H2’s viability as an alternative fuel source. We are eager to see the innovations that may come from these advancements and the hope is that responsible, clean H2 production from renewable energy resources will be prioritized. H2 production is still very energy intensive, so using fossil fuels to drive the process is not the answer to industrial decarbonization.

References

(1) Ajanovic, A.; Sayer, M.; Haas, R. The Economics and the Environmental Benignity of Different Colors of Hydrogen. Int. J. Hydrog. Energy 2022, 47 (57), 24136–24154. https://doi.org/10.1016/j.ijhydene.2022.02.094.

(2) Climate Solutions for EU Industry: Interaction between Electrification, CO2 Use and CO2 Storage; Zero emissions platform, 2019. https://zeroemissionsplatform.eu/wp-content/uploads/ZEP-report-Climate-solutions-for-EU-industry-interaction-between-electrification-CO2-use-and-CO2-storage-1.pdf.

(3) Roadmap to Decarbonising European Cars; 2018. https://www.transportenvironment.org/wp-content/uploads/2021/07/2050_strategy_cars_FINAL.pdf

(4) Hydrogen. https://www.irena.org/Energy-Transition/Technology/Hydrogen

(5) The Section 45Q Tax Credit for Carbon Sequestration; 2023. https://sgp.fas.org/crs/misc/IF11455.pdf.

(6) Credit for Carbon Oxide Sequestration. Federal Register. https://www.federalregister.gov/documents/2020/06/02/2020-11907/credit-for-carbon-oxide-sequestration

(7) Treasury Sets Out Proposed Rules for Transformative Clean Hydrogen Incentives | Clean Energy. The White House. https://www.whitehouse.gov/cleanenergy/clean-energy-updates/2023/12/22/treasury-sets-out-proposed-rules-for-transformative-clean-hydrogen-incentives/

(8) House, T. W. Biden-Harris Administration Announces Regional Clean Hydrogen Hubs to Drive Clean Manufacturing and Jobs. The White House. https://www.whitehouse.gov/briefing-room/statements-releases/2023/10/13/biden-harris-administration-announces-regional-clean-hydrogen-hubs-to-drive-clean-manufacturing-and-jobs/

(9) Hydrogen Industry Development Plan (2021-2035) – Policies. IEA. https://www.iea.org/policies/16977-hydrogen-industry-development-plan-2021-2035

(10) Hydrogen Leadership Roadmap – Policies. IEA. https://www.iea.org/policies/16975-hydrogen-leadership-roadmap

(11) Hydrogen Strategy – Policies. IEA. https://www.iea.org/policies/11721-hydrogen-strategy